Utilising blockchain technology to disrupt the insurance industry.

InsurTech startups are using blockchain technology to disrupt the insurance industry. The blockchain’s “smart contract” technology means that insurance policies can be written with less ambiguity and with fewer points of contention. It also enables both the insurers and the insured to verify the location of people and goods in the real world, enabling sophisticated and verifiable peer-to-peer operations in financial services. Consumer interest in this new technology is veritable, despite being a minority: an average of 38% of global consumers have either used a peer-to-peer service to borrow money or are interested in doing so. To the innovators, these blockchain-based insurance models present a way of re-establishing trust between insurers and their customers: the blockchain’s algorithm operates autonomously and cannot be manipulated by either party for gain. We rounded up the four insurtech disruptors that you need to know:

1. Dynamis

Basing their platform on Ethereum, a blockchain-based smart contract platform, Dynamis provides peer-to-peer unemployment insurance. Founded in late 2015, it provides supplemental unemployment insurance and severance coverage for small businesses, helping them provide the package in the case of layoffs or resignations. The company pays premiums into a de-centralised contract, setting up individual accounts for all its employees. If there are no claims, the premiums gradually go down. For employees, the account allows them to use the money while seeking employment and to transfer the details to their new workplace. This insurtech disruptor also asks users to verify their identity by connecting their account with their LinkedIn profile, where their employment history and searches are verified by their LinkedIn contacts.

2. Lemonade

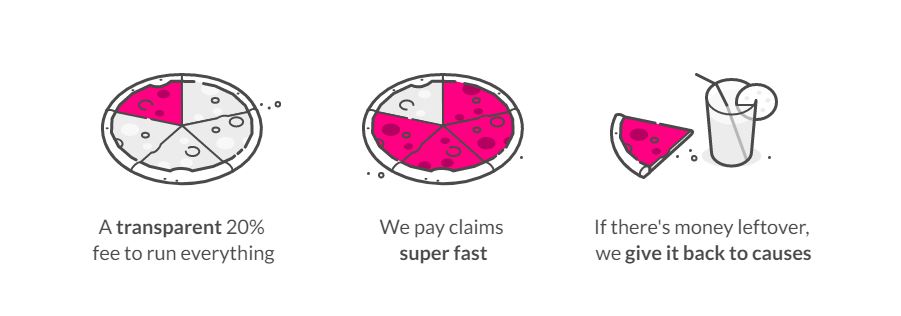

Lemonade launched in the US in late 2016, claiming to be the first peer-to-peer insurance company. Specialising in property and casualty insurance, their business model takes a fixed fee from monthly payments and uses an algorithm to pay out claims as soon as possible, when conditions in blockchain-based smart contracts are met. The startup also has a Giveback feature that uses the collected premiums from groups of peers to donate to a good cause.

3. InsurETH

This insurtech disruptor is also based on Ethereum and provides blockchain-based travel delay insurance. Founded in 2015, the disruptor offers automatically to users that it detects has flight delays, by using a blockchain algorithm. If a delay is registered, the app triggers an insurance claim, verified via the open blockchain data ledger, and automatically pays the user if the claim is proven correct.

4. Teambrella

Leveraging both the blockchain and a peer-to-peer concept, Russian start-up Teambrella lets users form “teams” that effectively insure each other. The teams pre-agree the insurance policy’s terms and conditions and, in case of claims, members vote on whether it is to be paid and on what level – the median of the team’s offers is then paid out to the claimant. The insurtech service’s main aim is to provide an insurance service alternative where the provider does not have an incentive to not pay out claims.

Interested in fintech disruptors? Read about inclusive finance here.